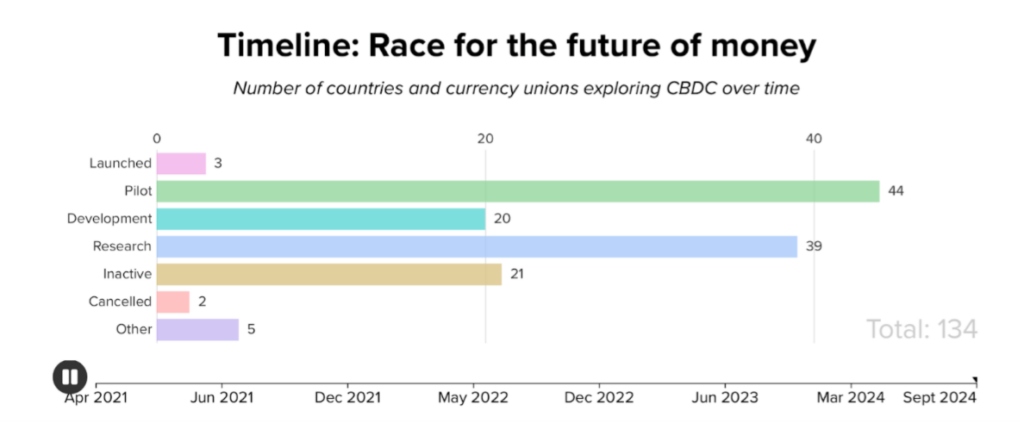

As 2025 begins, the future of Central Bank Digital Currency looks bright in Europe, Asia, Africa and South America, but not in the United States.. As 2024 came to a close, research from the Atlantic Council showed that 137 countries and currency unions — representing 98% of global GDP — were exploring a central bank digital currency (CBDC) in some form. Today, the Atlantic Council tracker show that there are over 44 CBDC pilots taking place with 20 additional countries working to develop pilots.

Why are CBDCs gaining traction outside of the United States?

CBDCs offer reliable sources of digital currency for consumers, businesses and governments. Unlike crypto currencies, CBDCs provide the same level of protection and insurance as fiat currencies do.

Although privacy and fear of government overreach continue to be debated, the regulation

and adoption of CBDCs continues to accelerate in many countries. Much of the debate over CBDCs as intrusive and lacking in privacy doesn’t include the fact that on the blockchain, permissions to access transactions can be permission controlled. In simple terms, this means that the permissions can provide privacy control.

The Trump White House Executive Order on CBDCs

Although the Trump White House has issued a recent executive order that cites the “risks” of central bank digital currencies, or CBDCs as threatening ” the stability of the financial system, individual privacy, and the sovereignty of the United States. ” outside the US, CBDC exploration and use is rising.

Indeed, many countries are adopting the technology for CBDCs to provide their citizens and those who can’t qualify for bank accounts based on employment status or income, with the ability to transact without bank account and transaction fees. This type of model in other countries promotes financial inclusion, accelerates payments, advances interoperability and significantly lowers banking fees for transactions. The recent Trump Executive Order leaves the CBDC field open to players outside of the US. It also favors private cryptocurrencies, which flood the market without meaningful regulation, or the protection that Central Bank Digital Currencies provide.

The world is digital, why shouldn’t money be?

Since the Covid-19 pandemic, the world has become digital and contactless. Today ,the majority of citizens use mobile phones and digital wallets to carry out financial transactions. There are increasingly more people who make payments with technology, rather than use a paper check book.

CBDC solutions, underpinned by blockchain technology, allow for integration with mobile apps, enabling greater financial inclusion for citizens, while simultaneously eliminating third-party banking fees. Current developments demonstrate that many of the world’s largest central banks are moving forward with plans to pilot and launch their own digital currencies to compliment existing fiat currencies.

Countries driving CBDC Innovation

While the recent White House Executive Order makes it clear that CBDCs are not moving forward in the United States, many other countries are at work on issuing Central Bank Digital Currencies.,

- China has issued their retail CBDC, the Digital Yuan, which is used directly by their people.India is working on their Digital Rupee.

- The Bahamas has successfully launched the first CBDC, the Sand Dollar and continues to enhance its marketing and awareness efforts to drive its use among their citizens.

- The Bank of Brazil is moving into Phase II of the DREX CBDC project.

- Under the umbrella of BRICs, 10 countries are working together on a CBDC including Russia, India, Iran, Egypt and South Africa.

- In Europe, The European Central Bank (ECB) is actively looking to transform the fiat Euro to a Digital Euro.

- The Bank of England recently published a “blueprint” for a Digital Pound. . This work is the precursor to developing a CBDC pilot, or a digital pound (CBDC.)

- The European Central Bank has progressed with pilots and designs to envision the key features of a future digital euro.

- In 2024, the Bank of Georgia completed Phase I of their Digital Lari project. At the time of this writing they are readying Phase II of the project.

- In Asia, The Hong Kong Monetary Authority (HKMA ) continues their pilots and efforts to drive the birth of a hypothetical e-HKD.

- In Africa, many nations are evaluating CBDCs with Nigeria having already released an e-Naira.

These facts demonstrate that the time is now for the advent of digital currencies backed by Central Banks. Because CBDCs can be managed, monitored, controlled and redeemed as needed by Central Banks, the implementation of these digital assets merits pilots and testing to establish trust and reliability.

Technology: Central Bank software as a service to enable CBDCs

A variety of technology companies offer a comprehensive platform for minting, managing, transacting and redeeming CBDCs. With blockchain technology and CBDC software, Central Banks now have the tools to mint, manage, transact, redeem and destroy CBDCs.

It’s expected that in 2025 there will be greater adoption of Central Bank Digital Currencies.The transformation from fiat to digital currencies offers the promise of lower costs for basic financial services, increased security, accelerated payments and reduced energy consumption.

When you consider these factors, as well as the audit trail that blockchain provides for tracking and tracing transactions, plus the backing of a digital currency by a nation’s Central Bank (which private cryptocurrencies don’t provide) it’s hard to ignore the benefit of a CBDC Central Bank Digital Currency, with all its inherent protections and insurance, is moving from vision to reality outside of the United States.

The question is, will Trump’s new Executive Order leave the US behind and allow other nations to lead in implementing CBDCs?